Beyond the Allowance: HNW Families

April 24, 2026

Money Management Apps, Teens, and the Unique Challenge of Raising Children in High Net Worth Families

If you’ve built real wealth, one question may keep High Net Worth (HNW) parents up at night.

It isn’t whether your kids will have enough.

It’s whether they’ll know what to do with it.

And will getting it too easily erode the traits that built it in the first place?

Money management apps are now practical, easy tools families use to teach financial skills in a cashless world.

But the apps commonly recommended — Greenlight, Acorns Early, BusyKid, Step — were designed for the mass-affluent family, not for the affluent household where a teenager already understands that "we can afford it.” For HNW families, picking the right tool is not about grocery budgets.

It is about creating structured, age-appropriate friction around money.

This helps kids build the judgment they will need later.

One day, they may steward a much larger balance sheet.

This article compares the leading teen money apps, highlights where each one fits (and doesn't) in a HNW household, and addresses the harder parenting question underneath it all: how do you raise a grounded, motivated child when almost nothing has to be earned?

The Parenting Problem Behind the App Decision

Before comparing features, it's worth naming what HNW parents are actually trying to solve for. The psychological literature on growing up wealthy — sometimes described colloquially as "affluenza" — points to a consistent cluster of risks: a diminished capacity to delay gratification, an inflated sense of entitlement, difficulty tolerating frustration, and, perhaps counterintuitively, higher-than-average rates of anxiety and depression in affluent adolescents.

These are not inevitable outcomes. They are, however, documented patterns.

These patterns show up when children are shielded from consequences. They also appear when money is seen as something that just exists. It is not seen as the result of work, choices, and trade-offs.

Three specific challenges show up repeatedly in HNW households:

1. The disappearance of natural consequences

In most families, a teenager who overspends runs out of money. In HNW families, the card gets topped up. Without deliberate design, kids can reach adulthood having never actually experienced a spending decision with teeth — which means they've never built the mental muscle to weigh one.

2. The "invisible" origin of wealth

When parents are successful enough that work happens in offices, on planes, or behind closed doors, children often have no felt sense of how money is generated. They see the outputs — homes, vacations, cars, the pool — but not the inputs. Over time this can produce adults who are comfortable with wealth but uncomfortable with the effort required to create or preserve it.

3. The values gap between generations

The parents in most HNW households today built their wealth. Their children are inheriting it. That shift — from creator to recipient — requires an entirely different skill set, and it rarely develops on its own. Financial literacy tools, when chosen thoughtfully, are one of the earliest and cheapest interventions a family can make.

These are the problems the right app helps address. They are also, importantly, the problems the wrong app can make worse — by reinforcing the idea that money is something that appears in a balance every week for doing very little.

What HNW Parents Should Consider

Most "best of" lists grade these apps on features like chore automation, card customization, and parental spending limits. Those matter, but they're table stakes. For families operating at a different altitude, the criteria worth weighing are:

• Whether the app supports real, age-appropriate investing — not just savings. Teens in HNW households will almost certainly interact with equities, ETFs, and eventually alternative investments as adults. Early, low-stakes exposure to market behavior is more valuable than another chore tracker.

• Whether parental controls are granular enough to create genuine structure (spending categories, merchant blocks, cash-back routing to savings or giving) without feeling like surveillance to a 16-year-old.

• Whether the app meaningfully teaches the mechanics of giving. For families who expect philanthropy to be part of their legacy, a "Give" bucket isn't a nice-to-have — it's a training ground.

• Whether the app scales up as kids mature. A tool that works for a 10-year-old but is patronizing to a 17-year-old just means switching platforms mid-stream.

• Whether the parental reporting is useful to you as an advisor-collaborator, not just as a parent. Spending data over time is a teaching asset.

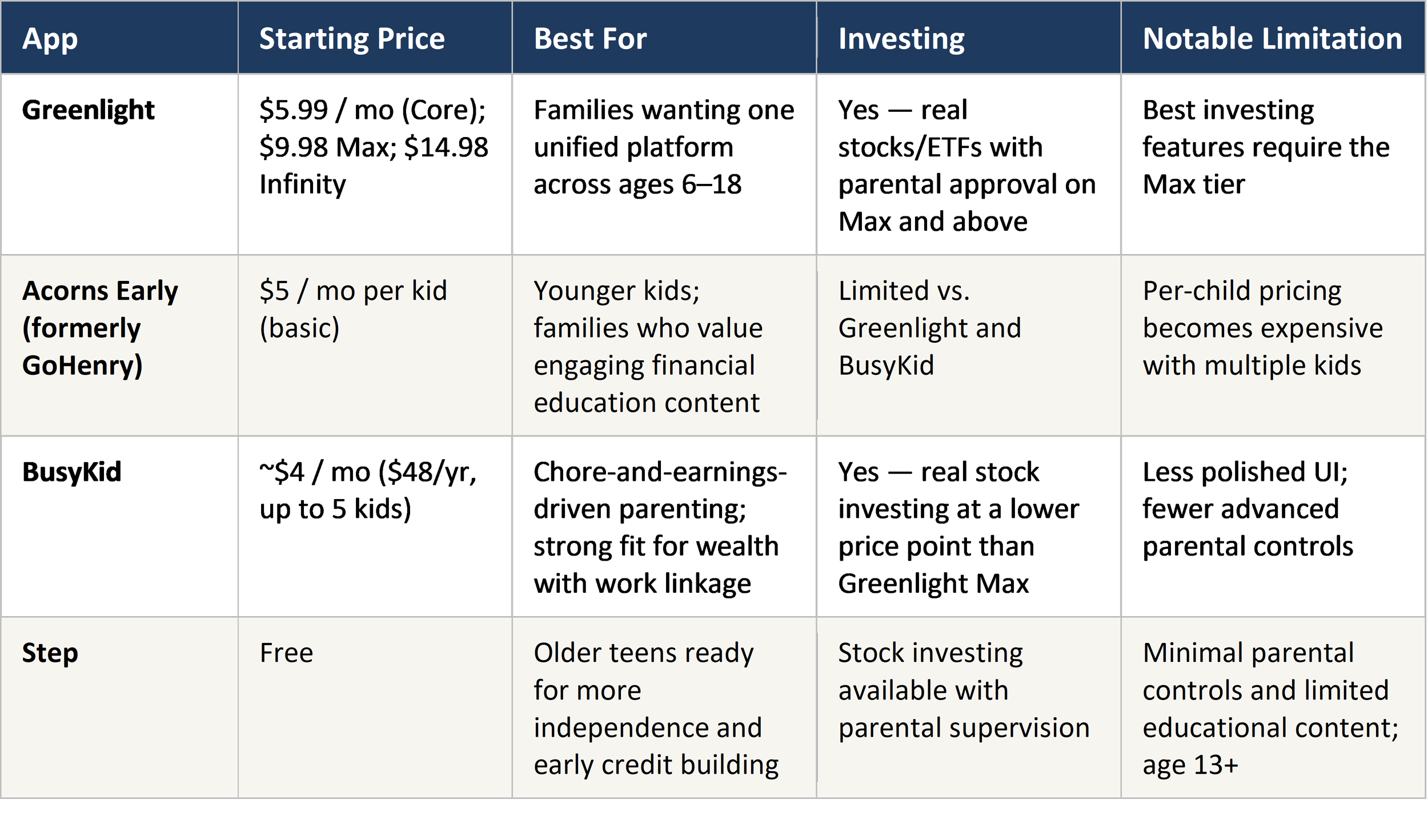

The Apps: A Side-by-Side Comparison

Four platforms dominate the teen money space in 2026, each with a different philosophy. Monthly pricing and features are current as of this writing; families should verify on each provider's site before committing.

Greenlight: A Popular Choice

Greenlight has become the category leader for a simple reason: it combines the widest feature set in one product. Within a single-family subscription, parents can automate allowance. They can tie specific chores to specific pay.

They can set spending limits for each merchant. They can see real-time purchase notifications. They can route roundups or paycheck portions into savings goals.

On the Max and Infinity tiers, teens can invest in real stocks and ETFs. Every trade requires parental approval.

For HNW families, Greenlight's appeal is structural. The Max tier's investing component is arguably the most valuable feature in the entire teen-app category: it creates a sandbox in which a 14- or 15-year-old can buy their first share of a public company, watch it move, and have a conversation with a parent about why it did. That conversation is the point. The app is just the vehicle.

Where Greenlight underdelivers for this demographic is in the depth of its investing education. Kids can buy shares, but the platform is not built to teach key investing basics.

It does not cover portfolio building, tax lots, or the difference between concentrated and diversified holdings.

A teen in a high-net-worth household will face these topics early.

This is even more true if they get gifted shares, UTMA payouts, or interests in family trusts. Greenlight is a strong starting point. It is not a substitute for an ongoing conversation with your advisor.

When Greenlight is the right call

• You want one platform across multiple kids of different ages.

• You value granular parental controls and real-time visibility.

• You're willing to pay for the Max tier to unlock investing — for most HNW families this is the only tier worth considering.

When another app may fit better

• Your family's teaching philosophy is strongly work-for-pay. BusyKid's chore-to-dollars architecture is more opinionated in that direction.

• Your teenager is 16+ and would benefit from a more adult-feeling experience. Step's free, direct-deposit-capable account with early credit building may be a better bridge to adulthood.

• You want a platform that actively gamifies financial literacy for younger kids. Acorns Early (formerly GoHenry) has stronger educational content for the 7–11 band.

How HNW Families Typically Layer These Tools

In practice, most of the HNW families I work with don't pick one app and stop there. They build a progression that matches the child's developmental stage and the family's teaching goals.

A common pattern looks something like this:

Ages 7–11: Earning and the idea of trade-offs

The goal at this stage is not financial sophistication. It is the basic emotional experience of choosing one thing over another with a finite resource. A chore-linked app (BusyKid or Acorns Early) establishes the connection between effort and reward. At this age, the dollar amounts should be small enough that spending decisions feel real.

Ages 12–15: Structure and the introduction of investing

This is where Greenlight Max tends to earn its price. Teens gain more autonomy, start making meaningful purchase decisions, and — critically — begin buying individual stocks with small amounts of their own money. The first time a 13-year-old watches a position drop 20 percent is a teaching moment that no parental lecture replicates.

Ages 16–18: Bridging to adult financial infrastructure

By this age, many teens are ready to move from a parent-controlled app to something more real. They may open a teen checking account like Step. They may also open a custodial brokerage account. An advisor can set it up as a UTMA.

If the teen has earned income, it may be a Roth IRA. Depending on the family’s situation, it also helps to talk about gifted securities.

It can also help to discuss tax-loss harvesting on custodial holdings. You can also explain what direct indexing looks like.

This is the handoff point where the app becomes a complement to — not a substitute for — professional financial planning.

The Conversations the Apps Can't Have For You

Even the best-designed app is a tool, not a philosophy. HNW parents who use these platforms most effectively treat them as the scaffolding for conversations they want to have anyway. A few that matter most:

Where our money comes from

Children who understand the source of family wealth — the business that was built, the career that compounded, the risks that were taken — tend to relate to that wealth more responsibly than children for whom money simply appears. This conversation does not require disclosing balances. It requires disclosing the story.

What our money is for

Values determine allocation. Families who articulate what wealth is meant to accomplish — security, education, generational stability, philanthropy, freedom to do work that matters — give their children a framework for making their own financial decisions later. Without that framework, adult inheritors often default to consumption.

What we expect of you

One of the most protective factors in affluent families is clear, consistent expectation-setting. Money apps can help operationalize this: a teen who knows the family rule is "50 percent of earned money goes to savings or investing" internalizes a pattern that will outlast the app by decades.

What happens if you make a mistake

HNW teens need, more than most, to be allowed to make small financial mistakes. A depleted Greenlight balance at age 14 is inexpensive tuition. A depleted trust distribution at age 34 is not. The goal of these apps is not to prevent every bad decision — it's to create a safe environment for bad decisions to happen while the stakes are still low.

The Bottom Line

Greenlight, Acorns Early, BusyKid, and Step are all considered credible tools. For most HNW families with multiple kids, Greenlight Max is a strong starting point. It fits families who want one well-integrated platform. Its real investing feature is the key benefit. It is the highest-leverage teaching tool in this category.

Families with a strong chore-for-pay philosophy should consider BusyKid. Older teens benefit from the more grown-up feel of Step.

But the app matters less than what the family does with it. The children of HNW parents are, on average, going to inherit far more complexity than the typical American household ever navigates — multiple account types, concentrated positions, trust structures, tax considerations, philanthropic vehicles, and in many cases operating businesses. The teen money app is the first rung on that ladder. It is not the ladder itself.

That work—the real work of raising financially capable adults—happens at the kitchen table over years. It happens in partnership with the advisors, attorneys, and accountants your family already trusts. The apps are just a useful place to start the conversation.

Disclosure: This article is provided for educational purposes and does not constitute investment, tax, or legal advice. Product features, tiers, and pricing for third-party apps mentioned herein are based on publicly available information as of the date of writing and are subject to change; readers should verify current terms directly with each provider. Mention of any product does not constitute an endorsement or recommendation. Please consult your advisor, tax professional, and attorney before making financial decisions for your family. All information contained herein is derived from sources deemed to be reliable but cannot be guaranteed. All views/opinions expressed in this newsletter are solely those of the author and do not reflect the views/opinions held by Advisory Services Network, LLC.

Sources:

• Greenlight Help Center, "What fees are associated with Greenlight?" — help.greenlight.com/hc/en-us/articles/4404247122587

• Greenlight, "Compare Plans" — greenlight.com/plans

• Greenlight Help Center, "How much does the Greenlight Infinity plan cost?" — help.greenlight.com/hc/en-us/articles/10383447981723

• Acorns Early / GoHenry, "GoHenry is becoming Acorns Early" — gohenry.com/us/blog/news/gohenry-is-becoming-acorns-early

• BusyKid Help Center, "Annual Cost" — helpcenter.busykid.com/hc/en-us/articles/26657448008212

• BusyKid, Frequently Asked Questions — busykid.com/common-faqs

• MoneyRates, "Step Teen Checking Review 2026" — moneyrates.com/checking/step-teen-checking-review.htm

• MyBankTracker, "Step Teen Banking Account 2026 Review" — mybanktracker.com/checking/reviews/step-card-teen-banking-account-review-432126

• FinanceBuzz, "Acorns Early (GoHenry) vs. Greenlight [2026]" — financebuzz.com/gohenry-vs-greenlight

• FinanceBuzz, "Greenlight Debit Card Review [2026]" — financebuzz.com/greenlight-review

• Finder, "BusyKid vs. Greenlight" — finder.com/kids-banking/busykid-vs-greenlight

• Bankrate, "4 best money apps for teaching kids financial literacy" — bankrate.com/personal-finance/best-money-apps-for-kids

• WalletHub, "4 Best Budgeting Apps for Teens in 2026" — wallethub.com/answers/b/budgeting-apps-for-teens-2140878684