Vesting Explained: 401(k) Vesting Schedules & Stock Benefits

March 20, 2025

Many employers enhance compensation packages with benefits such as company stock awards or contributions to workplace retirement plans in addition to base pay. These incentives are designed to help recruit and retain skilled employees.

However, employees do not always gain full ownership of these benefits immediately. Instead, they may be subject to vesting rules, which determine when the employee earns the right to keep employer-provided contributions, stock, or other incentives. Understanding vesting is important when evaluating job offers and comparing benefits packages.

What Is Vesting?

Vesting refers to the process through which an employee gradually earns ownership of benefits provided by an employer. These benefits may include retirement plan contributions, company stock awards, or certain cash incentives. Depending on the plan’s structure, ownership may be granted all at once, accumulate over time, or depend on meeting specific performance goals.

If an employee leaves the company before satisfying the vesting requirements, they may lose some or all of the employer-provided benefits.

Retirement plans often include vesting schedules for employer contributions. For example, an employer may match a portion of the employee’s contributions to a 401(k). While the employee’s own contributions are always theirs, the employer match may only become fully owned after a specified period of service.

How Vesting Works

Employers establish the vesting schedule for their benefits programs. In many cases, vesting is tied to how long an employee remains with the company.

For instance, a company may grant stock as part of its compensation package but require employees to remain employed for a certain number of years before gaining full ownership. Whether the benefit comes in the form of retirement contributions, company stock, or other incentives, employees typically earn a larger share over time until they eventually reach full ownership.

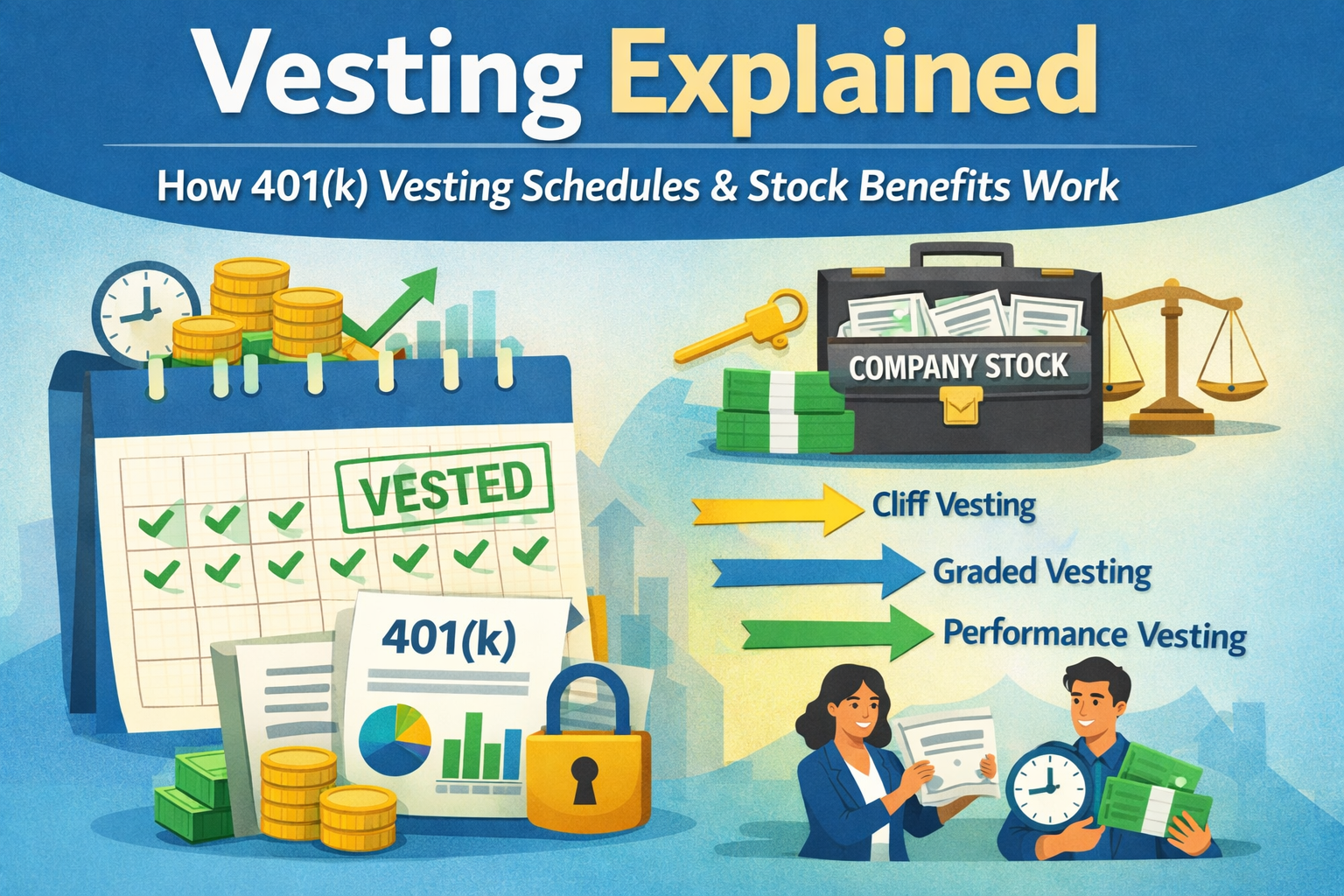

Common Vesting Structures

Several vesting approaches are commonly used by employers.

Graded Vesting

Under graded vesting, ownership increases gradually over a defined period. For example, a five-year schedule might allow employees to earn 20% ownership each year. After one year, the employee would be 20% vested; after two years, 40%; continuing until reaching full ownership at the five-year mark.

Cliff Vesting

Cliff vesting involves a waiting period before any ownership is granted. In a three-year cliff schedule, for example, employees gain full ownership only after completing three years of service. Leaving the company before that point typically means forfeiting the benefit.

Some plans combine cliff vesting with gradual vesting afterward. For example, a four-year schedule with a one-year cliff might grant 25% ownership after the first year and the remaining portion over the next three years.

Performance-Based Vesting

In some cases, vesting depends on meeting specific goals rather than simply remaining employed. Companies may tie stock awards to revenue targets, profit benchmarks, or individual performance metrics.

Immediate Vesting

Certain employer contributions become the employee’s property right away. When a plan offers immediate vesting, there is no waiting period to gain ownership.

Vesting in a 401(k)

Within a 401(k) plan, vesting generally applies only to employer contributions. Money that employees contribute from their own paychecks is always theirs to keep.

For example, imagine an employee contributes $40,000 to their 401(k) over several years, and the employer contributes an additional $1,000. If the plan uses a three-year cliff schedule and the employee leaves before reaching three years of service, they would keep their own $40,000 but forfeit the employer’s $1,000 contribution.

With graded vesting, the employee might retain a portion of those employer contributions depending on how long they remained with the company.

Certain events can accelerate vesting. If a retirement plan is terminated or an employee reaches the plan’s defined retirement age, they may automatically become fully vested in employer contributions.

Tax Treatment of Vested Contributions

Employer contributions to a traditional 401(k) are generally not taxed when they vest. Instead, taxes are owed when the funds are withdrawn during retirement.

In a Roth 401(k), employees make after-tax contributions. Employer contributions are typically deposited into a pre-tax portion of the account and taxed upon withdrawal. However, under newer rules introduced by recent legislation, some employers may choose to deposit contributions into an after-tax Roth account, which could create taxable income in the year the contribution is made.

Vesting and Equity Compensation

Vesting rules also apply to various types of stock-based compensation.

Restricted stock units (RSUs), for example, represent a promise to deliver company shares—or their cash value—once vesting conditions are met. When the shares are delivered at vesting, the value is treated as taxable income.

Stock options and stock appreciation rights (SARs) often follow vesting schedules as well. Options allow employees to purchase company stock at a predetermined price, while SARs provide compensation based on increases in the company’s stock price. Taxes are typically triggered when the option is exercised or when gains are realized.

What Is a Vested Balance?

A vested balance represents the portion of employer-provided benefits that the employee fully owns. Once benefits are vested, they cannot be taken back by the employer even if the employee leaves the company.

As vesting progresses over time, the vested balance increases until the employee owns the full value of the employer’s contributions or awards.

What It Means to Be Fully Vested

Being fully vested means the employee has met all requirements to claim the entire benefit. At that point, they own 100% of the employer-provided contributions or equity awards associated with the plan.

In some retirement plans, becoming fully vested may also allow employees to retain future employer contributions immediately, though this depends on the plan’s rules.

Why Vesting Matters

Vesting schedules can significantly affect the real value of a compensation package. When evaluating job offers, it’s helpful to review how long it takes to become fully vested in employer contributions or stock awards.

A benefit that appears generous may be less valuable if the vesting schedule requires many years of service. Since career paths can change unexpectedly, there is always a possibility of leaving before the benefits fully vest.

If questions arise about how vesting schedules or related taxes work, consulting a financial or tax professional may help clarify the details.

Sources:

https://www.fidelity.com/learning-center/smart-money/vesting

Disclosure:

This information is an overview and should not be considered as specific guidance or recommendations for any individual or business.

This material is provided as a courtesy and for educational purposes only.

These are the views of the author, not the named Representative or Advisory Services Network, LLC, and should not be construed as investment advice. Neither the named Representative nor Advisory Services Network, LLC gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your Financial Advisor for further information.