When Should You Refinance? Factors to Consider

April 17, 2026

Anyone who’s purchased a home in the past few years has likely been watching interest rates closely, waiting for an opportunity to improve their financing. After the unusually low mortgage rates seen during the pandemic—often below 3%—the jump to the 6%–7% range has been a significant adjustment for many buyers.

Now that rates have started to ease from their recent highs, homeowners who bought or refinanced at higher levels may be asking a practical question: is it time to revisit their mortgage?

The answer depends on a mix of financial variables, not just where rates stand today.

What it means to refinance a mortgage

Refinancing involves replacing your current home loan with a new one. The new mortgage pays off the existing balance, and you begin making payments under a new set of terms.

Homeowners typically refinance to secure a lower interest rate, but that’s not the only reason. A refinance can also allow you to adjust the length of your loan, change loan types, or access home equity.

How the process works

When you refinance, you apply for a new mortgage much like you did when you originally bought your home. Once approved, the new loan replaces the old one entirely.

The updated loan may come with different terms—such as a lower rate, a shorter or longer repayment period, or even additional cash if you’re tapping into your equity. However, refinancing isn’t cost-free. Closing costs, lender fees, and the time required to complete the process all need to be factored into the decision.

When refinancing starts to make sense

At its core, refinancing is a math problem. The key question is whether the long-term savings from a lower rate outweigh the upfront costs of getting the new loan.

For illustrative purposes only.

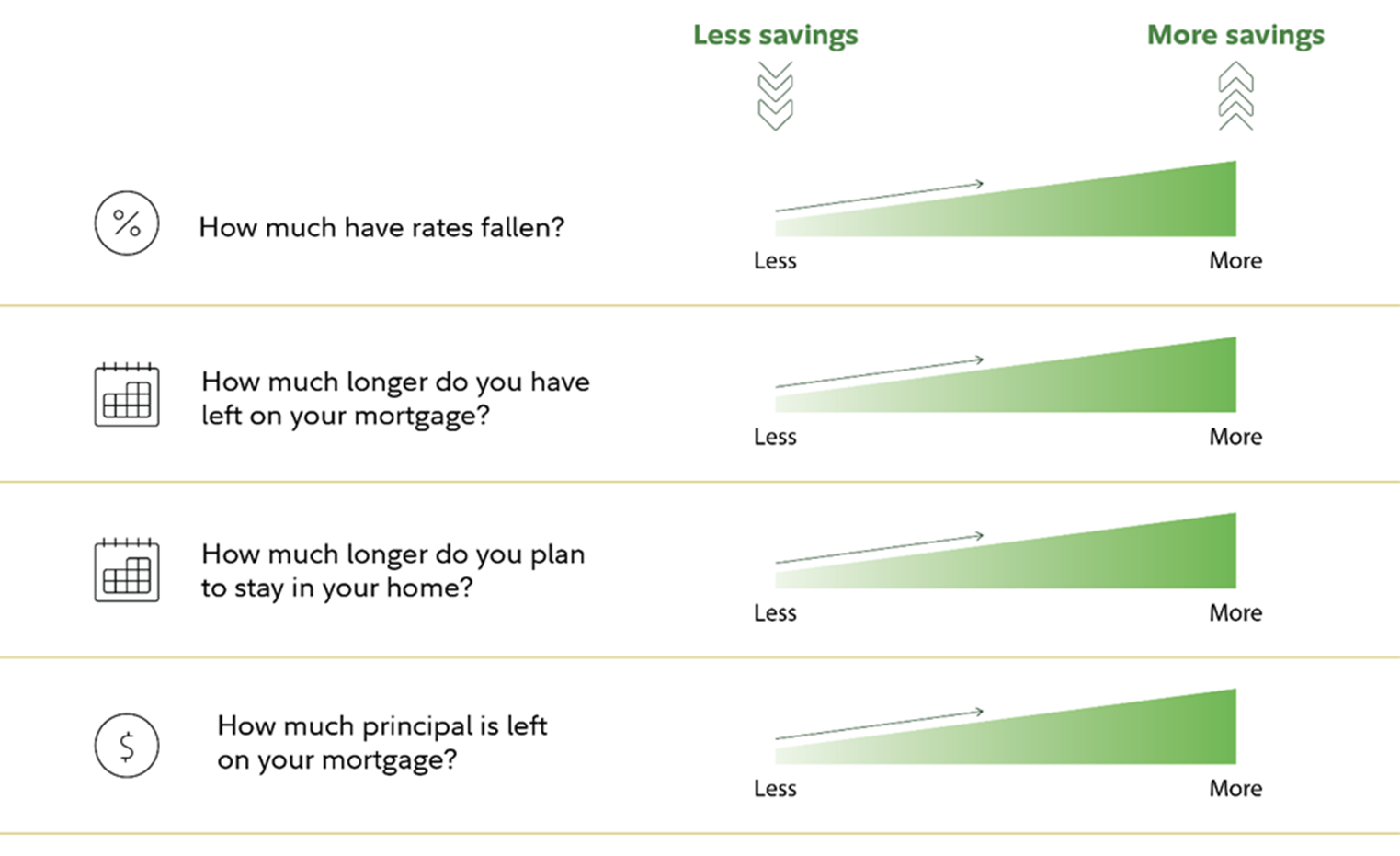

Several factors drive that calculation:

1. The size of the rate drop

The larger the decline in interest rates, the greater the potential savings. You may also qualify for better terms if your credit profile has improved since you first took out your mortgage.

2. Time remaining on your loan

Even a modest rate reduction can lead to meaningful savings over many years. But if you’re near the end of your mortgage, there may not be enough time left to justify the costs.

3. How long you plan to stay in the home

If you expect to move in the near future, refinancing may not pay off. On the other hand, a longer time horizon increases the likelihood that savings will exceed costs.

4. Your remaining loan balance

A higher outstanding balance generally increases the potential benefit of refinancing, since the interest savings apply to a larger amount.

Understanding the cost side

One of the most overlooked aspects of refinancing is the expense involved. Closing costs can vary, but they often fall in the range of roughly 3% to 6% of the loan amount. These costs reduce—or in some cases eliminate—the financial benefit of a lower rate if you don’t hold the loan long enough.

That’s why many homeowners look at a “break-even point,” or how long it takes for monthly savings to recover those upfront costs.

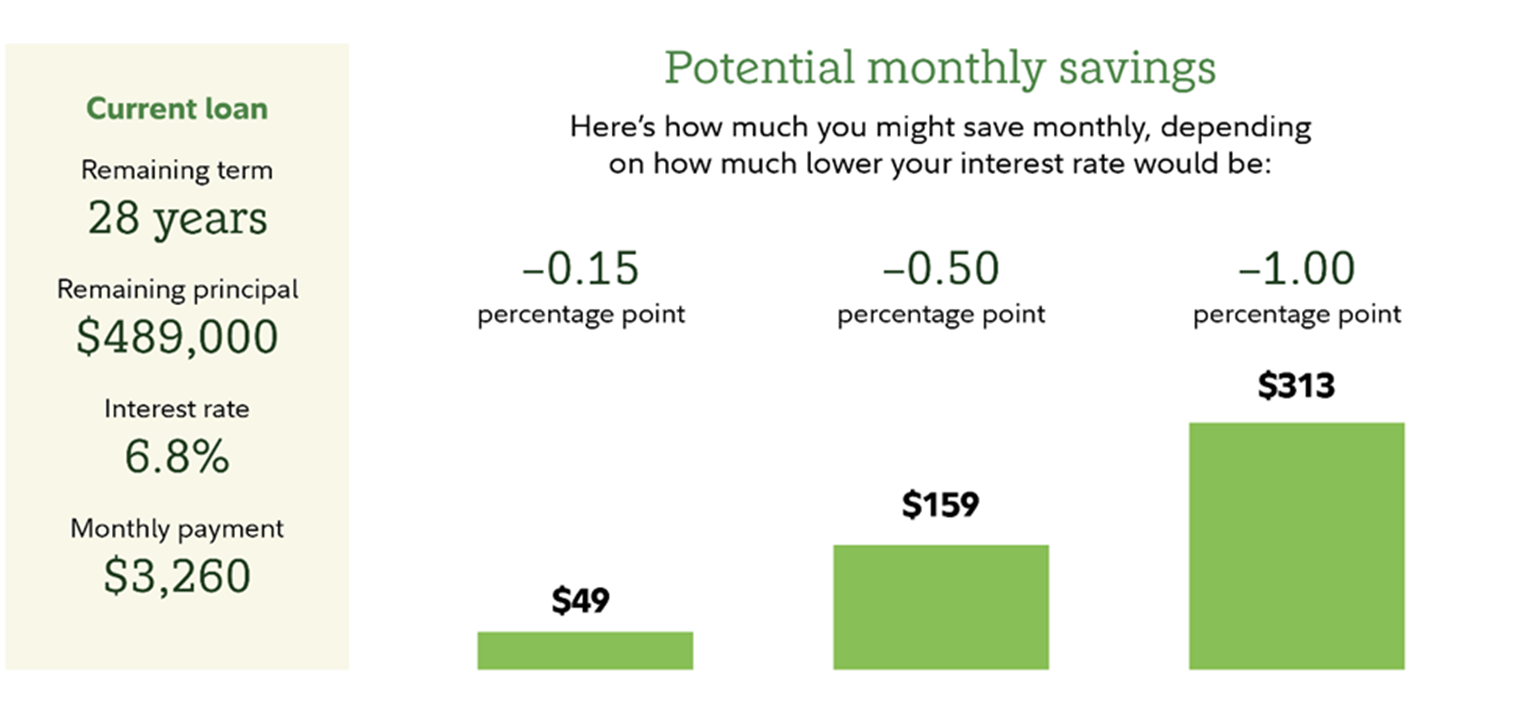

Here’s an example of how monthly savings could play out for a homeowner refinancing to secure a lower interest rate, assuming they keep the same loan term and aren’t taking any cash out of their equity.

Figures are hypothetical and for illustrative purposes only. New mortgage is assumed to be for 28-year term and $489,000 balance. Figures do not consider the impact of closing costs. Source: Fidelity.

The numbers make it clear: the larger the drop in interest rates, the more you stand to save each month. That said, refinancing comes with costs—most notably closing expenses and the time involved in securing a new loan. The real decision comes down to whether the long-term interest savings are enough to outweigh those upfront costs.

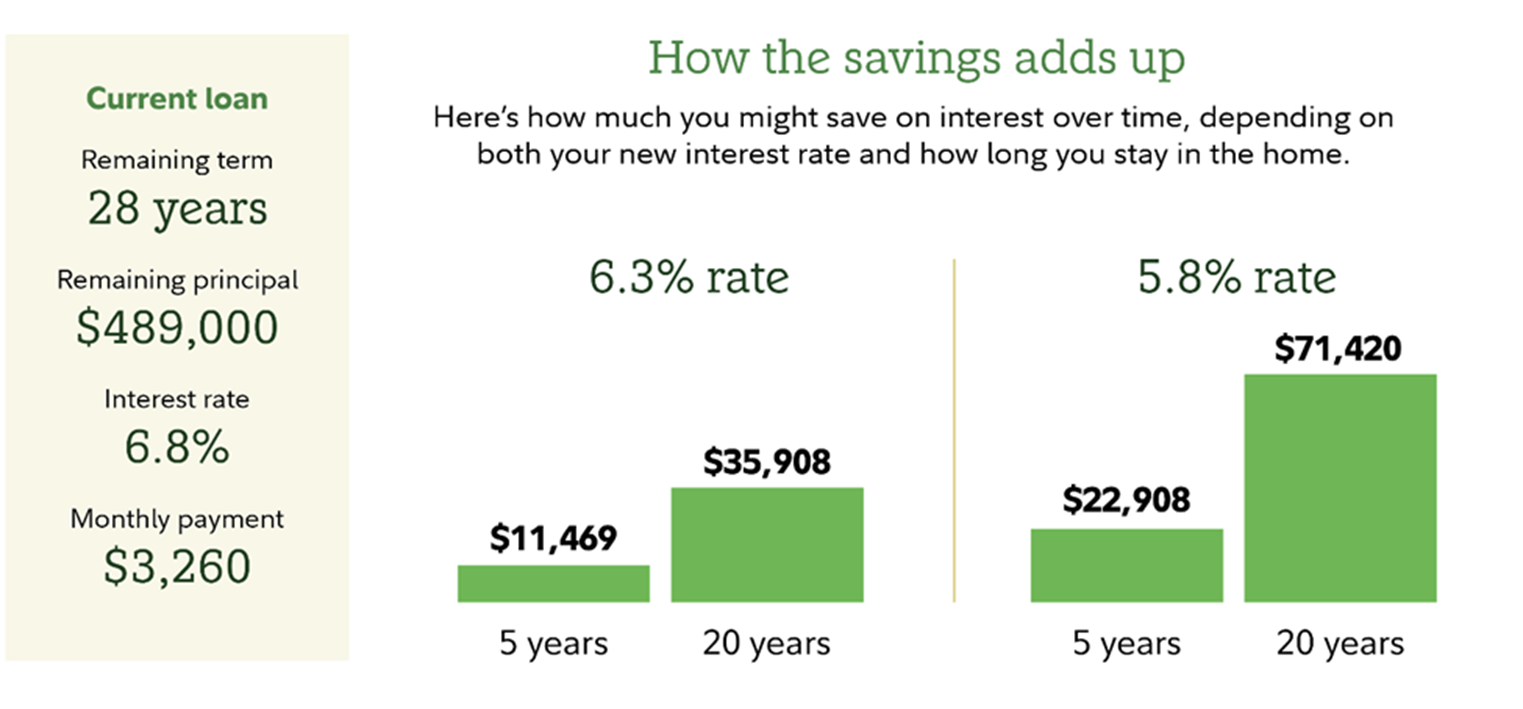

How much could you actually save?

Savings can vary widely depending on your loan size, interest rate reduction, and how long you keep the mortgage.

Imagine you’re two years into a 30-year mortgage that began with a $500,000 balance at a 6.8% interest rate. Your potential interest savings from refinancing—measured in today’s dollars—will vary based on the new rate you qualify for and how long you plan to remain in the home.

Figures are hypothetical and for illustrative purposes only. New mortgages are assumed to be for 28-year term and $489,000 balance. Estimated savings represent present value of total savings over the stated time period, discounted to a present value using a 2.5% inflation assumption. Figures do not consider the impact of closing costs. Source: Fidelity.

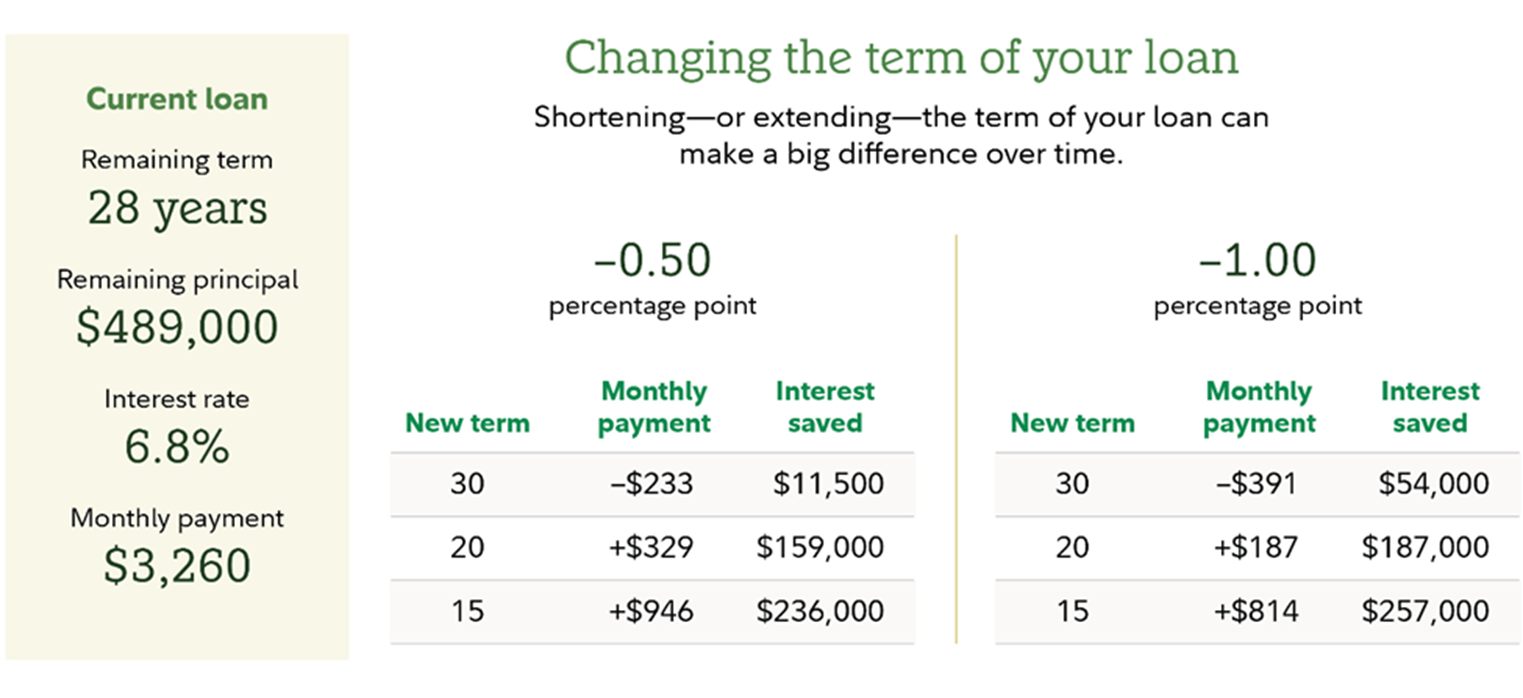

Changing your loan term

Refinancing doesn’t have to be a like-for-like swap. Adjusting the loan term can significantly impact both monthly payments and total interest paid.

● Shorter term: Typically comes with lower rates and less total interest, but higher monthly payments.

● Longer term: Reduces monthly payments but may increase total interest over time.

The right choice depends on your cash flow and broader financial priorities, including saving and investing.

Negative change in monthly payment indicates a decrease, while positive change in monthly payment indicates an increase. Figures are hypothetical and for illustrative purposes only. Borrower is assumed to stay in home for the remainder of the mortgage term. Source: Fidelity.

What is a cash-out refinance?

A cash-out refinance allows you to borrow more than your current mortgage balance and receive the difference in cash. This effectively converts a portion of your home equity into usable funds.

Lenders usually cap how much you can borrow based on your home’s value, often limiting loans to around 80% of the property’s worth. While the funds can be used for a variety of purposes, it’s important to weigh the long-term cost of increasing your mortgage balance.

The bottom line

Refinancing isn’t something you need to evaluate every time rates move. But if rates have declined meaningfully—and you expect to stay in your home for several years—it may be worth running the numbers.

The most effective approach is straightforward: estimate your potential monthly savings, compare that to your closing costs, and determine how long it will take to come out ahead.

If the numbers work in your favor, refinancing can be a practical way to reduce interest costs, improve cash flow, or reposition your mortgage to better align with your broader financial strategy.

Sources:

https://www.fidelity.com/learning-center/personal-finance/refinance-mortgage

Disclosure:

This information is an overview and should not be considered as specific guidance or recommendations for any individual or business.

This material is provided as a courtesy and for educational purposes only.

These are the views of the author, not the named Representative or Advisory Services Network, LLC, and should not be construed as investment advice. Neither the named Representative nor Advisory Services Network, LLC gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your Financial Advisor for further information.