Maturing CDs and Bonds: Reinvestment Strategies

April 28, 2026

Holding cash in a portfolio is like a temporary guest. It is useful for a specific purpose. But you do not want it to linger without a clear reason.

When interest rates hit their highest levels in decades, many investors picked short-term choices. These included CDs and Treasury securities. Now that rates have eased, those same investors are encountering a new challenge: what to do as those investments mature. Reinvesting at lower yields may feel unattractive, but shifting into higher-return opportunities often introduces additional risk.

Rather than rushing into your next investment, it’s often better to step back. Evaluate how this part of your portfolio fits your broader financial picture. Asking the right questions can help bring clarity.

1. What purpose does this money serve?

Start by defining the goal. Is this money earmarked for a home purchase, emergency reserves, education funding, or retirement? The intended use should guide your next move.

If the objective is already clear, align your strategy accordingly. For example, education savings may fit a dedicated college savings account, while retirement funds may go into an IRA. Remember contribution limits.

If there’s no defined purpose, it may be worth establishing one. Consider if your emergency fund is enough, if you should reduce debt, or if the money can support a long-term goal. Clarifying intent often leads to more disciplined investment decisions.

2. How should it be invested for that goal?

Once the objective is set, evaluate how to allocate the funds. Factor in your timeline and risk tolerance. Then see how this money fits with other assets set aside for the same purpose.

Short-term goals—like a home purchase within a couple of years—may warrant more conservative vehicles such as short-duration bonds or CDs. Longer-term objectives, like retirement a decade or more away, may allow for greater exposure to growth-oriented investments. For those nearing retirement, structuring income through bond or CD ladders may be appropriate.

3. How does it fit into your overall portfolio?

Zoom out and assess your full asset allocation across accounts. What proportion is in equities, fixed income, and cash?

If your portfolio has drifted out of alignment, these maturing funds can be an opportunity to rebalance. Many investors hold too much cash or very safe assets. This can limit growth and reduce purchasing power over time due to inflation. Conversely, investors approaching or in retirement may intentionally favor income-producing, lower-volatility holdings.

There’s no universal formula—the right mix depends on your goals, time horizon, and risk profile.

4. How liquid should it be—and how much risk is acceptable?

If you decide to remain in fixed income, two variables become central: access to your money and your comfort with risk.

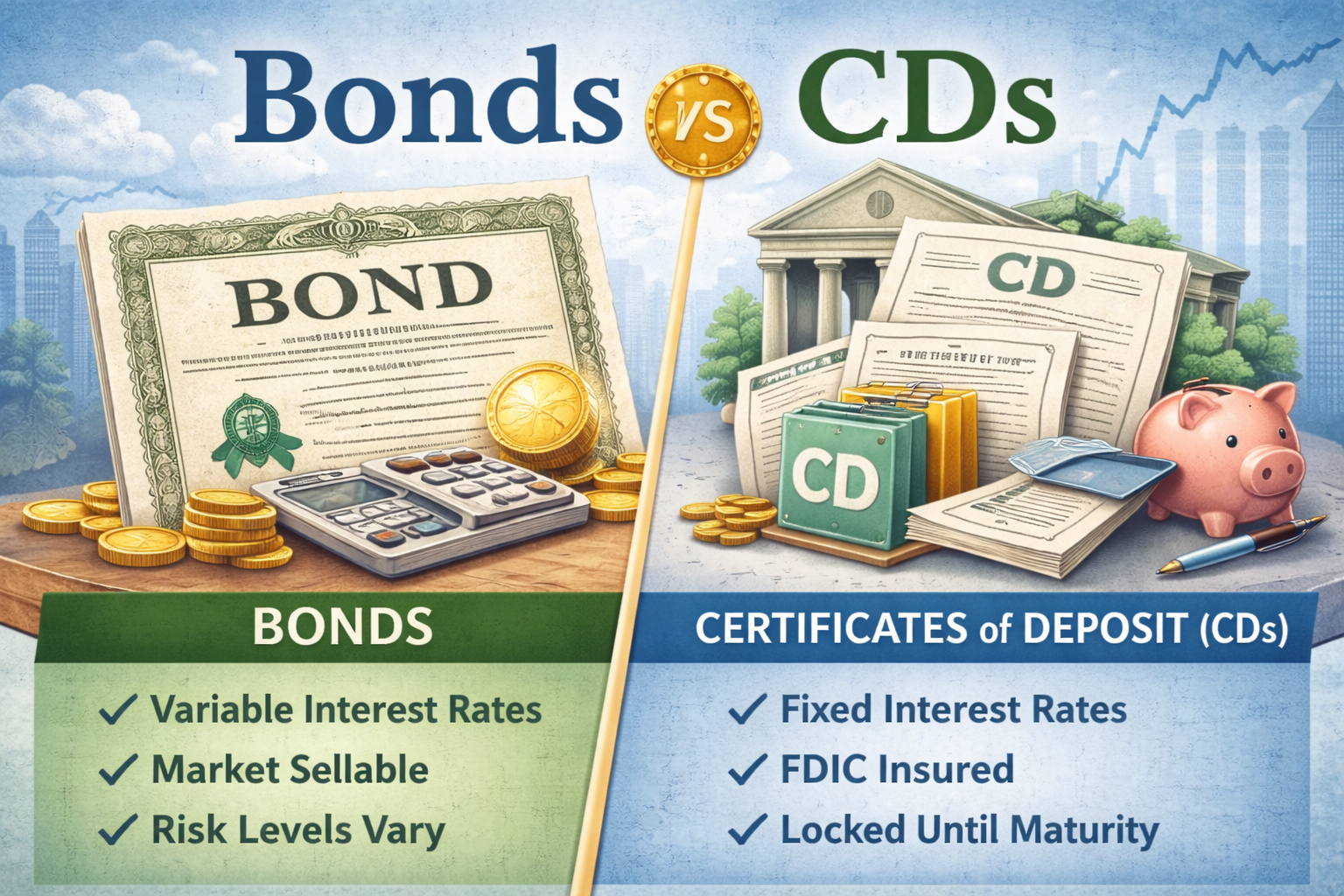

● CDs offer low risk and FDIC insurance (within limits), but typically require you to hold funds until maturity unless you’re willing to sell early, potentially at a loss.

● Money market funds provide liquidity and yields that tend to track short-term rates, though they are not FDIC-insured and carry some risk.

● Bonds span a wide spectrum. U.S. Treasurys are generally considered low risk, while corporate and municipal bonds vary depending on issuer quality. Short-term bonds tend to be less sensitive to rate changes, while longer-term bonds may offer higher yields but with greater price volatility.

Each option involves tradeoffs—there isn’t a single “best” choice, only what aligns most closely with your needs.

5. How hands-on do you want to be?

Finally, consider how actively you want to manage these assets.

Owning individual CDs or bonds requires periodic decisions as they mature. Some investors value that level of control, while others prefer a more streamlined approach.

More hands-off alternatives include:

● Bond funds or ETFs, where professional managers handle security selection and reinvestment

● Annuities, which can provide predictable income streams, particularly for retirees

● Automatic reinvestment services, which roll proceeds from maturing securities into new ones without requiring constant oversight

Bringing it together

While the number of choices may feel overwhelming, the decision becomes more manageable when anchored to your objectives, time horizon, and preferences. Instead of focusing only on where to reinvest, use this moment to check your strategy. Ensure it still aligns with your long-term plan.

If the process feels complex, working with a financial advisor can help translate these moving parts into a clear, actionable strategy.

Sources:

https://www.fidelity.com/learning-center/trading-investing/maturing-cds

Disclosure:

This information is an overview and should not be considered as specific guidance or recommendations for any individual or business.

This material is provided as a courtesy and for educational purposes only.

These are the views of the author, not the named Representative or Advisory Services Network, LLC, and should not be construed as investment advice. Neither the named Representative nor Advisory Services Network, LLC gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your Financial Advisor for further information.