Roth IRA Conversions: Tax Strategies, Timing, and Key Rules

February 27, 2026

Shifting assets from a pre-tax retirement account—such as a traditional 401(k) or traditional IRA—into a Roth 401(k) or Roth IRA can offer meaningful long-term advantages. The tradeoff is straightforward: you owe ordinary income tax on the amount converted. In exchange, future qualified withdrawals from the Roth account are tax-free. That tax treatment can enhance flexibility in retirement income planning and potentially increase after-tax cash flow.

Historically, Roth IRAs have not been subject to required minimum distributions (RMDs) during the original owner’s lifetime. Beginning in 2024, Roth 401(k)s receive similar treatment, eliminating lifetime RMDs for account owners. This change enhances their value in both tax management and estate planning strategies.

Why consider a Roth conversion now?

There are several strategic reasons to evaluate a conversion this year or next.

Market volatility can create opportunity. If equity markets decline, converting when account values are temporarily lower may reduce the immediate tax cost, since the taxable amount is based on the value converted at the time of the transaction.

Current tax rates may not last forever. Even though recent legislation made existing federal income tax brackets permanent, future policy changes are always possible. Converting at today’s rates may reduce lifetime tax exposure if rates increase down the road. It also creates the potential for tax-free distributions in retirement and may eliminate future RMD obligations from the converted funds.

If a Roth conversion seems appealing, here are answers to several frequently asked questions. As always, consult a qualified tax advisor before proceeding.

Can I convert a traditional 401(k) to a Roth 401(k)?

Yes—provided your employer-sponsored plan offers a Roth feature and permits in-plan conversions. Taxes will generally apply to any pre-tax amounts converted.

Can I convert a traditional 401(k) to a Roth IRA?

Yes. If you are retired, you can roll assets directly from a traditional 401(k) to a Roth IRA. If you are still employed, the plan must allow in-service withdrawals. You may complete the conversion through a direct rollover into a Roth IRA or first roll funds into a traditional IRA and then convert to a Roth IRA.

What if my income is too high to contribute to a Roth IRA?

Income limits restrict direct Roth IRA contributions, but they do not apply to conversions. High earners may contribute to a traditional IRA (even if the contribution is nondeductible) and then convert those funds to a Roth IRA. This strategy is commonly referred to as a “backdoor” Roth contribution.

How is the tax on a Roth conversion calculated?

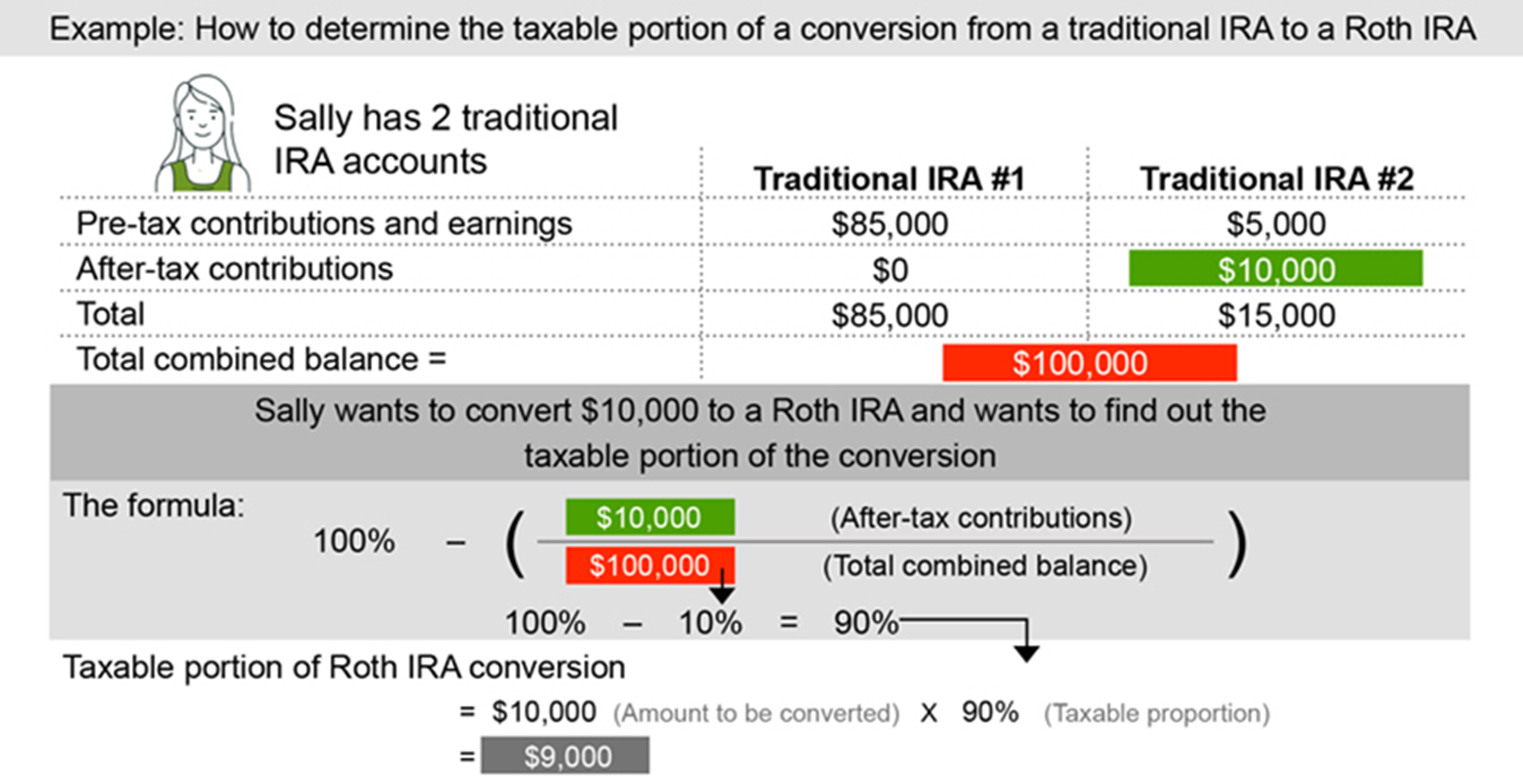

For tax purposes, all traditional IRAs you own—excluding inherited IRAs—are aggregated and treated as a single IRA. Your tax liability depends on:

1. The portion of the conversion that is taxable income

2. Your marginal tax rate

Traditional IRA contributions fall into two categories:

● Deductible (pre-tax) contributions – Contributions that reduced your taxable income in the year made.

● Nondeductible (after-tax) contributions – Contributions for which no tax deduction was taken. These create “basis” in the IRA.

If you have never made nondeductible contributions, the entire converted amount is generally taxable.

If you have both deductible and nondeductible amounts, the IRS requires a proportional calculation. You cannot isolate only after-tax dollars for conversion. Instead, you determine the percentage of your total IRA balances that represents after-tax contributions and apply that percentage to the conversion amount to calculate the non-taxable portion.

Keep in mind:

● Investment earnings are always taxable upon conversion.

● Inherited IRAs are excluded from the aggregation rule.

● State income taxes may also apply.

Because each spouse’s IRAs are calculated independently, couples sometimes consider converting the spouse whose IRAs contain a higher proportion of after-tax contributions first.

This hypothetical example is for illustrative purposes only. It shows how to figure out what part of an IRA conversion is taxable income.

Are there ways to offset the tax impact?

Certain deductions may help mitigate the tax cost. Charitable contributions, for example, can be deductible if you itemize. Cash donations to qualified charities are generally deductible up to 60% of adjusted gross income (AGI), while some other contributions may be limited to 30% of AGI.

However, if your total itemized deductions do not exceed the standard deduction, you may not receive a tax benefit. Coordinating charitable giving with a Roth conversion requires careful planning.

Does timing during the year matter?

A conversion must be completed by December 31 to count for that tax year.

Converting early in the year provides more time to prepare for the tax bill, which is generally due by the following April tax deadline (though estimated tax payments may be required sooner).

Converting later in the year offers two potential advantages:

● The IRS five-year rule begins on January 1 of the conversion year, regardless of the actual conversion date. Each conversion has its own five-year holding period to avoid penalties on converted principal.

● You’ll have clearer insight into your total annual income, making it easier to convert only enough to stay within a desired tax bracket.

Can I convert specific investments rather than selling them?

Yes. You may transfer securities “in kind” from a traditional IRA to a Roth IRA. From a tax perspective, it makes no difference whether you convert cash proceeds or transfer the investment itself—the fair market value at the time of conversion determines the taxable amount.

Bottom Line

A Roth conversion can be a powerful component of a long-term tax strategy, but it is not universally appropriate. The decision should incorporate projected income, current and future tax brackets, estate planning goals, and available cash to pay the tax liability. A coordinated review with a financial and tax professional is essential before implementing a conversion strategy.

Sources:

Disclosure:

This information is an overview and should not be considered as specific guidance or recommendations for any individual or business.

This material is provided as a courtesy and for educational purposes only. A ROTH Conversion is a taxable event. Consult your tax advisor regarding your situation.

These are the views of the author, not the named Representative or Advisory Services Network, LLC, and should not be construed as investment advice. Neither the named Representative nor Advisory Services Network, LLC gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your Financial Advisor for further information.