Strategies to Help Manage Inflation

April 29, 2026

Manage Inflation

Just as inflation seemed to be easing, it picked up again. Consumer prices in the U.S. climbed 3.3% year over year in March, with rising energy costs playing a major role. Gas prices alone have increased by roughly $1 per gallon compared to last year, putting renewed pressure on household budgets.

In an environment like this, managing inflation often requires a dual approach: tightening up everyday spending while positioning your investments to outpace rising costs over time.

10 Strategies to Help Manage Inflation

A thoughtful plan should address both your cash flow and your long-term portfolio.

1. Understand where inflation is hitting you most

Inflation isn’t evenly distributed—costs like housing, food, insurance, and transportation often rise faster than average.

Action steps:

● Review the past few months of spending to identify increases

● Focus on trimming higher-cost categories like groceries, fuel, and utilities

● Reassess regularly, as inflation pressures can shift

Pinpointing where costs are rising allows for more targeted adjustments.

2. Stabilize expenses when possible

Frequent price increases can make budgeting feel unpredictable.

Action steps:

● Negotiate recurring bills such as phone, internet, and insurance

● Consider locking in rates or using autopay discounts

● For housing, explore fixed-rate options or renegotiate lease terms early

Reducing variability in key expenses can provide more financial stability.

3. Strengthen your emergency fund

Cash reserves are essential—but inflation can erode their value over time.

Action steps:

● Maintain 3–6 months of essential expenses in reserve

● Keep excess cash in vehicles that may offer higher yields, like high-yield savings or short-term Treasurys

Balancing liquidity with return potential helps preserve purchasing power.

4. Maintain growth exposure in your portfolio

Over the long term, equities have historically been one of the more effective ways to outpace inflation.

Action steps:

● Ensure your asset allocation reflects your goals and time horizon

● Younger investors may lean more heavily into stocks

● More conservative investors may need to be intentional about maintaining growth exposure

Growth assets play a key role in offsetting inflation over time.

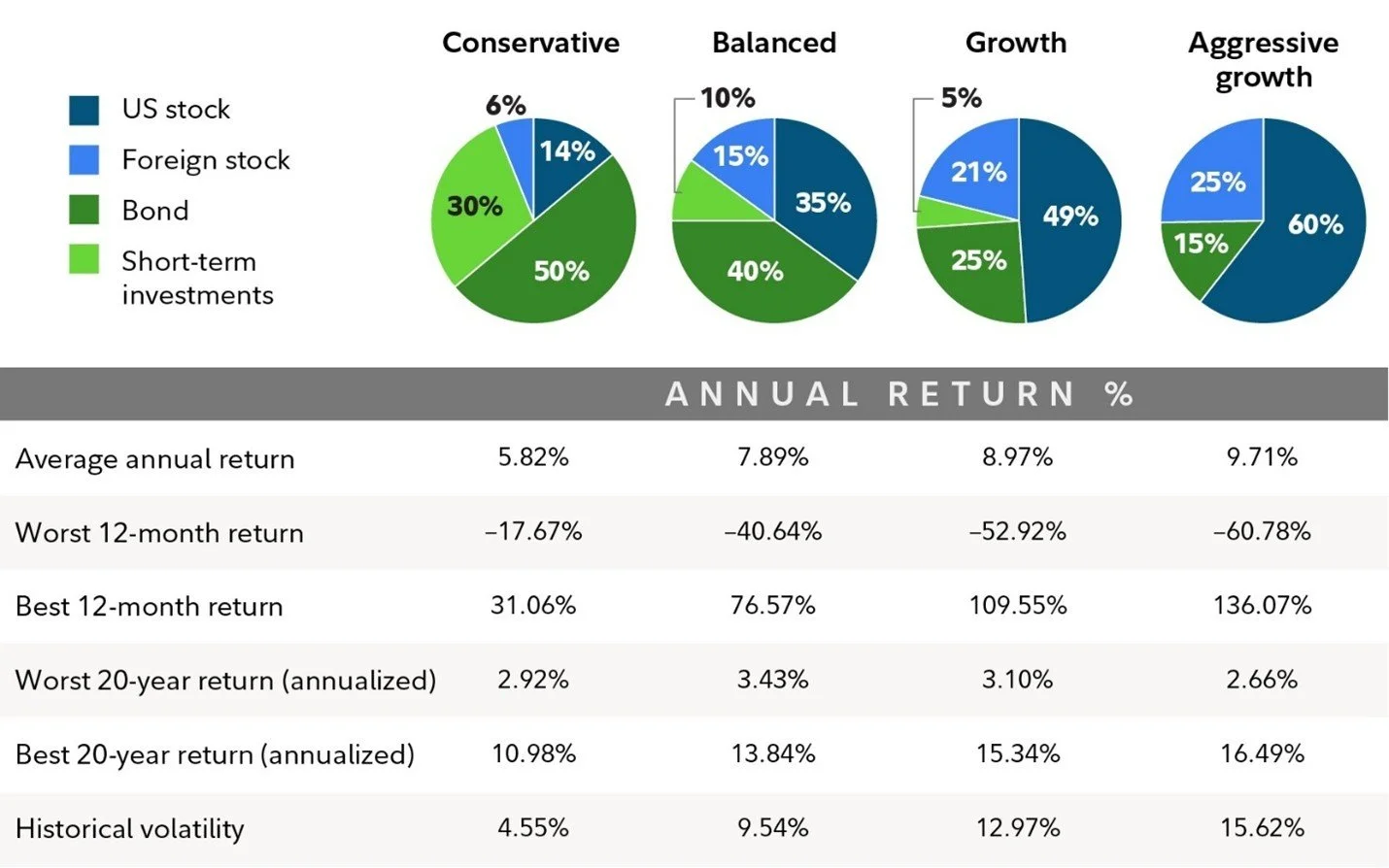

Annual Return Percentages

Data source: Fidelity Investments and Morningstar Inc, 2025 (1926–2025). Past performance is no guarantee of future results. Returns include the reinvestment of dividends and other earnings. This chart is for illustrative purposes only. It is not possible to invest directly in an index. Time periods for best and worst returns are based on calendar year. For information on the indexes used to construct this table, see Data Source in the notes below. The purpose of the target asset mixes is to show how target asset mixes may be created with different risk and return characteristics to help meet an investor’s goals. You should choose your own investments based on your particular objectives and situation. Remember, you may change how your account is invested. Be sure to review your decisions periodically to make sure they are still consistent with your goals.

5. Incorporate inflation-sensitive investments

Certain asset classes have historically performed better during inflationary periods.

Consider:

● Commodity-related stocks (energy, materials)

● Value-oriented equities

● Real estate investments, including REITs

● Inflation-linked bonds like TIPS

● Diversifiers such as gold

A diversified mix can help cushion against rising prices.

6. Be mindful with bond exposure

Rising inflation and interest rates can weigh on traditional bonds.

Action steps:

● Limit exposure to long-duration bonds, which are more rate-sensitive

● Consider shorter-term bonds or inflation-protected securities

● Align bond holdings with your income needs and risk tolerance

Bonds still serve a purpose—but their role may shift in inflationary periods.

7. Diversify globally

Inflation trends and economic cycles vary across countries.

Action steps:

● Add international investments to broaden diversification

● Reduce reliance on a single economy

● Consider managed portfolios that incorporate global exposure

International assets can help smooth returns over time.

8. Avoid overcommitting to inflation hedges

Not all inflation protection strategies are created equal.

Key considerations:

● Assets like gold may preserve value but don’t generate income

● Overweighting hedges can limit long-term growth potential

● A balanced allocation is typically more effective than extremes

The goal is resilience—not perfection.

9. Plan carefully in retirement

Inflation can be especially challenging once you’re no longer earning income.

Action steps:

● Rely on inflation-adjusted income sources when possible

● Consider delaying Social Security to increase benefits

● Keep part of your portfolio invested for growth

● Revisit withdrawal strategies regularly

A flexible income strategy is essential in retirement.

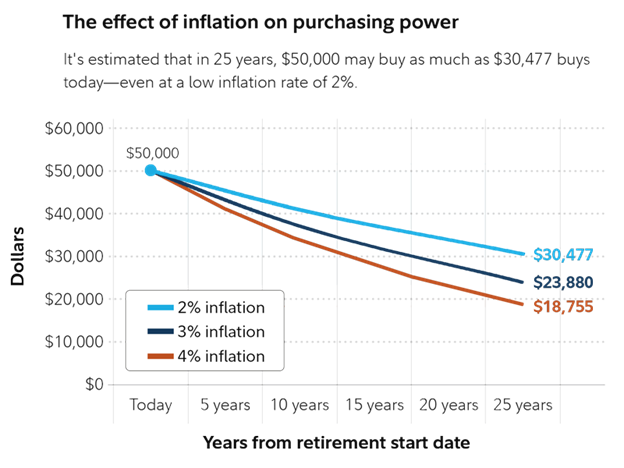

Inflation and Purchasing Power

Source: Fidelity Investments. All numbers were calculated based on hypothetical rates of inflation of 2%, 3%, and 4% (historical average from 1976 to 2025 was 3.6%) to show the effects of inflation over time; actual inflation rates may be more or less and will vary.

10. Review and adjust regularly

Inflation is dynamic, and your plan should be too.

Action steps:

● Periodically review your budget and investments

● Rebalance your portfolio as allocations drift

● Adjust based on changing economic conditions and life events

Consistency and adaptability are key to staying ahead.

Bottom Line

Inflation may be unpredictable, but your response doesn’t have to be. By combining disciplined spending with a clear investment plan, you can protect your buying power. You can also stay on track with your long-term financial goals.

Sources:

https://www.fidelity.com/learning-center/personal-finance/how-to-beat-inflation

Disclosure:

This information is an overview and should not be considered as specific guidance or recommendations for any individual or business.

This material is provided as a courtesy and for educational purposes only.

These are the views of the author, not the named Representative or Advisory Services Network, LLC, and should not be construed as investment advice. Neither the named Representative nor Advisory Services Network, LLC gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your Financial Advisor for further information.