Term vs. Whole Life Insurance: Understanding the Differences

May 21, 2026

Life insurance plays an important role in protecting the people who matter most to you. Whether the goal is replacing income, paying off debts, funding education costs, or leaving behind a financial legacy, the right policy can provide valuable peace of mind.

One of the biggest decisions individuals face when shopping for life insurance is choosing between term life insurance and whole life insurance. While both provide a death benefit to beneficiaries, they work very differently and are designed for different financial objectives.

Understanding how each type of coverage works can help you determine which approach best fits your needs.

What Is Term Life Insurance?

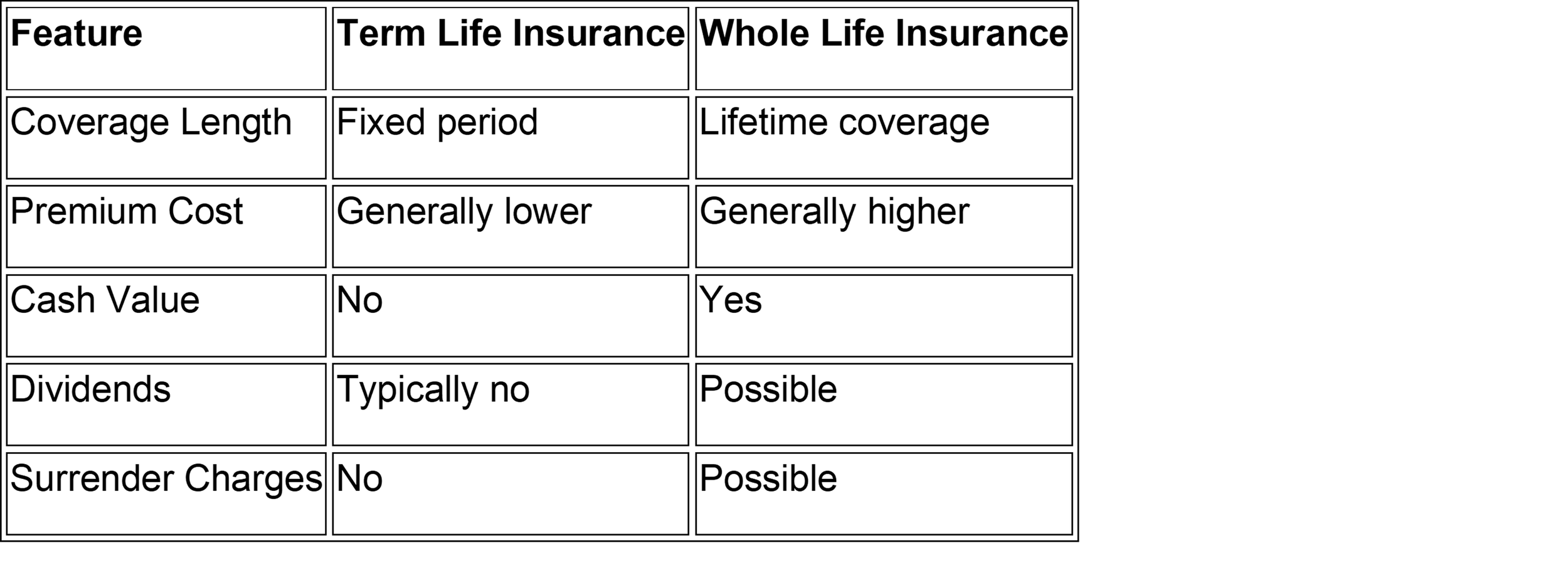

Term life insurance provides coverage for a specific period of time, commonly 10, 20, or 30 years. If the insured passes away during that term and premiums are current, beneficiaries generally receive an income-tax-free death benefit.

Once the term expires, coverage ends unless the policy is renewed or converted to another type of insurance. If the policy lapses or is not renewed, no benefit is paid.

Because term policies are temporary and do not build cash value, they are typically the most affordable type of life insurance.

What Is Whole Life Insurance?

Whole life insurance is a form of permanent life insurance designed to remain in force for the insured’s lifetime, provided premiums are paid.

In addition to offering a death benefit, whole life policies include a cash value component that grows over time. Policyholders may be able to access this cash value through withdrawals or policy loans, although doing so can reduce the death benefit.

Some whole life policies may also pay dividends, which can be used to:

● Increase cash value

● Purchase additional coverage

● Offset premiums

● Be taken as cash

Unlike term insurance, whole life coverage does not expire after a set number of years.

Similarities Between Term and Whole Life Insurance

Although they serve different purposes, term and whole life insurance share several common features.

Death Benefit Protection

Both types of insurance provide beneficiaries with a generally income-tax-free payout if the insured passes away while coverage is active.

Fixed Premium Structure

Most policies offer fixed premium payments. However, term insurance premiums often rise significantly if coverage is renewed later in life, while whole life premiums generally remain level.

Underwriting Requirements

Both policy types commonly require underwriting, which may include:

● Medical history reviews

● Prescription history checks

● Lifestyle evaluations

● Possible medical exams

Insurance companies use this information to determine eligibility and pricing.

Optional Riders

Many policies allow optional add-ons, commonly known as riders, that customize coverage. Examples may include:

● Conversion riders

● Accidental death benefits

● Waiver of premium riders

● Long-term care riders

● Return-of-premium features

These additions typically increase the policy cost but may enhance flexibility and protection.

Grace Periods

Both term and whole life insurance policies often include a grace period — commonly around 30 days — allowing missed premiums to be paid before coverage lapses.

Major Differences Between Term and Whole Life Insurance

While the two policy types share some similarities, the key distinctions are important when evaluating long-term financial goals.

Coverage Duration

The most obvious difference is how long coverage lasts.

Term life insurance is temporary and designed for a defined timeframe. Whole life insurance is intended to provide lifelong protection.

Cost Differences

Term life insurance generally offers significantly lower premiums because coverage is temporary and does not accumulate cash value.

Whole life insurance costs more because it combines permanent insurance protection with a savings component.

For some individuals, the higher cost may be justified by the policy’s long-term guarantees and cash accumulation features.

Cash Value Accumulation

Whole life insurance builds cash value over time. A portion of each premium contributes to this savings component, which grows tax-deferred.

Policyholders may access the cash value in several ways:

● Policy loans

● Withdrawals

● Using cash value to help pay premiums

● Surrendering the policy

It is important to understand that loans and withdrawals may reduce the final death benefit.

Term life insurance does not accumulate cash value.

Dividends and Policy Growth

Some participating whole life policies may pay dividends annually, although dividends are never guaranteed.

These dividends can help increase:

● Cash value growth

● Total death benefit

● Overall policy flexibility

Term policies generally do not offer dividends.

Surrender Charges

Whole life insurance may include surrender charges if the policy is canceled early. These fees are typically highest during the early years of the policy and gradually decline over time.

Term insurance does not involve surrender charges because there is no cash value component.

Who Might Benefit From Term Life Insurance?

Term life insurance is often appropriate for individuals seeking affordable protection during key financial years.

Common uses include:

● Replacing income for dependents

● Covering a mortgage balance

● Funding college education expenses

● Protecting against temporary financial obligations

For example, parents with young children may choose a 20-year term policy to help ensure education and living expenses are covered if something unexpected happens.

Who Might Benefit From Whole Life Insurance?

Whole life insurance may be better suited for individuals with long-term or permanent planning objectives.

Potential uses include:

● Estate planning strategies

● Leaving a tax-efficient legacy

● Providing lifelong support for dependents with special needs

● Creating liquidity for estate taxes

● Supplementing retirement income through policy cash value

Because whole life insurance remains in force for life, it can provide certainty regardless of when death occurs.

How Much Life Insurance Do You Need?

Coverage needs vary significantly from person to person.

A common guideline for term life insurance is maintaining coverage equal to roughly 10 to 12 times annual income, although factors such as debt, future education costs, and family needs should also be considered.

For whole life insurance, the appropriate amount often depends on broader estate planning goals, wealth transfer objectives, and long-term affordability.

Choosing the Right Policy

The decision between term and whole life insurance depends on your financial priorities, budget, and long-term goals.

Term life insurance may make sense for those seeking:

● Lower-cost coverage

● Temporary financial protection

● Simplicity

Whole life insurance may appeal to those looking for:

● Permanent coverage

● Cash value accumulation

● Estate planning benefits

● Long-term financial flexibility

In many cases, individuals use a combination of both types of insurance as part of a comprehensive financial plan.

Final Thoughts

Life insurance is about more than simply replacing income. It can serve as an important tool for protecting family members, preserving wealth, supporting long-term financial goals, and creating peace of mind.

Whether term or whole life insurance is the better fit depends on your unique circumstances, financial responsibilities, and future objectives. Reviewing your options carefully and evaluating how coverage fits into your broader financial strategy can help ensure your loved ones remain protected for years to come.

Sources:

https://www.fidelity.com/learning-center/personal-finance/term-life-vs-whole-life-insurance

Disclosure:

This information is an overview and should not be considered as specific guidance or recommendations for any individual or business.

This material is provided as a courtesy and for educational purposes only.

These are the views of the author, not the named Representative or Advisory Services Network, LLC, and should not be construed as investment advice. Neither the named Representative nor Advisory Services Network, LLC gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your Financial Advisor for further information.